Understanding the Basics of Insurance

Introduction to Insurance

Insurance is a mechanism that provides individuals, families, and businesses with financial protection against unexpected events and potential losses. It acts as a safety net, allowing people to transfer the risk of potential financial hardships to an insurance company in exchange for regular premium payments. In the event of an insured loss, the insurance company compensates the policyholder or beneficiary based on the terms and conditions outlined in the insurance policy.

Insurance plays a critical role in protecting individuals and businesses from a wide range of risks. It allows people to manage risks associated with their health, life, property, vehicles, businesses, and more. Insurance coverage can vary significantly depending on the type of policy and the specific risks being covered.

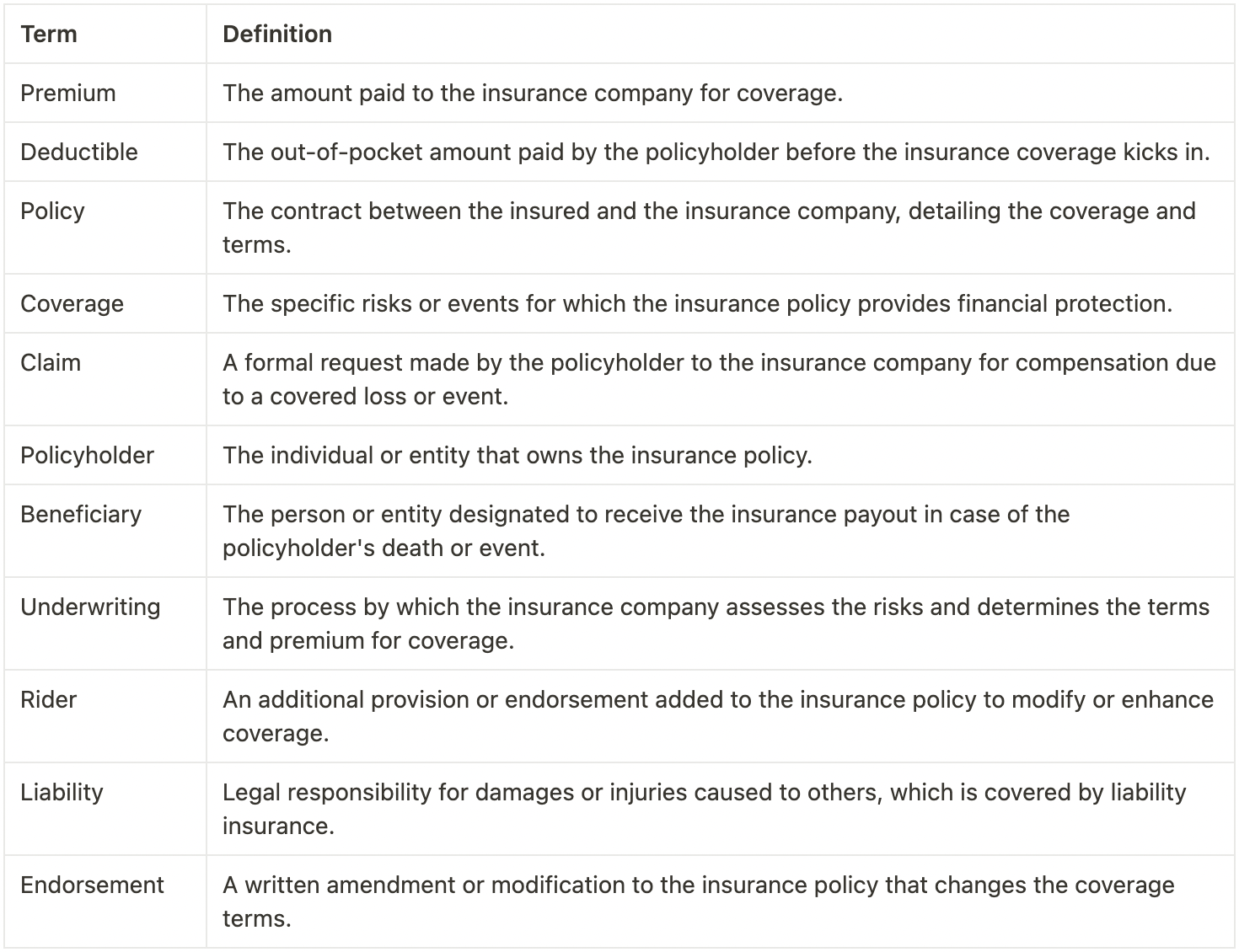

💡Common Insurance Terminology You Should Know

Importance of Insurance in Financial Planning:

Mitigating Financial Risks

- Insurance is a crucial risk management tool for transferring potential financial risks to an insurance company.

- It protects individuals and businesses from unforeseen events leading to significant financial losses.

Providing Financial Security

- Insurance provides a safety net for individuals and families, offering financial stability during challenging times.

- In the event of a loss, insurance policies can help cover expenses, such as medical bills, property repairs, or legal costs.

Safeguarding Assets and Investments

- Insurance helps protect valuable assets, such as homes, vehicles, businesses, and personal belongings.

- By safeguarding assets, Insurance preserves the financial value of investments and allows individuals to recover more quickly from setbacks.

Protecting Loved Ones' Future

- Life insurance plays a vital role in protecting the financial well-being of dependents in the event of the policyholder's death.

- It provides beneficiaries with a lump sum or regular payments, ensuring they can maintain their lifestyle, pay debts, and cover future expenses.

Promoting Long-Term Financial Goals

- Insurance aligns with long-term financial planning objectives by safeguarding wealth and preserving financial stability.

- By managing risks through insurance, individuals can focus on building and growing their assets without constantly fearing unforeseen events.

Life Insurance: Securing Your Loved Ones' Future:

- Life insurance is a financial safety net for your loved ones in the event of your passing.

- It provides a tax-free payout, known as the death benefit, to your beneficiaries.

Choosing the Right Coverage

- Evaluate your financial needs, such as income replacement, mortgage payments, education expenses, and debts.

- Consider the number of dependents, their age, and their future financial obligations.

- Assess your budget and determine the premium amount you can comfortably afford.

- Consult with a financial advisor or insurance agent to analyze your specific circumstances.

Beneficiaries and Estate Planning

- Designate primary and contingent beneficiaries on your life insurance policy.

- Regularly review and update beneficiary designations to ensure they align with your wishes.

- Consider the impact of estate taxes and consult an estate planning professional to maximize the benefits for your beneficiaries.

Home Insurance: Protecting Your Property and Belongings

Coverage Options:

Dwelling Coverage

- This covers the structure of your home, including walls, roof, foundation, and attached structures like garages and protects against damages caused by fire, vandalism, storms, and other covered perils.

Personal Property Coverage

- This coverage safeguards your belongings, such as furniture, appliances, electronics, and clothing and provides reimbursement for repairing or replacing items damaged or stolen due to covered perils.

Additional Living Expenses Coverage

- If your home becomes temporarily uninhabitable due to a covered event, this coverage helps with additional living expenses. It covers costs like hotel stays, meals, and other necessary accommodations during displacement.

Important Considerations:

- Coverage Limits: Ensure your dwelling coverage adequately reflects the estimated home rebuilding cost.

- Deductibles: A deductible is paid out of pocket before insurance coverage kicks in.

- Home Security and Safety Measures: Installing security systems, smoke detectors, and fire alarms can help reduce your premiums.

Health Insurance: Ensuring Access to Quality Healthcare:

Health insurance is a critical component of a well-rounded financial plan, providing protection against high medical costs. It ensures that individuals and families can access quality healthcare services without financial hardships.

Critical Components of Health Insurance Policies:

a. Coverage for Medical Expenses:

- Health insurance policies cover various medical expenses, including hospitalization, surgeries, doctor visits, prescription drugs, and laboratory tests.

b. In-Network Providers and Out-of-Network Options:

- Visiting in-network providers results in lower out-of-pocket costs, as insurers have agreements.

- Some plans may also offer out-of-network coverage, allowing individuals to seek care from providers outside the network, albeit at higher costs.

c. Deductibles, Copayments, and Coinsurance:

- Deductibles are the amount individuals must pay out of pocket before the insurance coverage starts.

- Copayments are fixed fees paid during service, such as a flat fee for doctor visits or prescription drugs.

- Coinsurance refers to the percentage of the medical costs individuals are responsible for, typically after meeting the deductible.

d. Maximum Out-of-Pocket Expenses:

- Health insurance policies often have a maximum out-of-pocket limit, beyond which the insurer covers all eligible expenses.

- Once this limit is reached, individuals no longer have to pay coinsurance or copayments, providing financial protection against catastrophic medical costs.

Insurance Claims Process: What to Expect

Assess the Situation:

- Determine the extent of the damage or loss.

- Take immediate steps to prevent further damage.

- Document the incident with photos, videos, and witness statements.

Notify Your Insurance Company:

- Report the incident promptly to your insurance company.

- Provide policy details and a description of what occurred.

Assign a Claims Adjuster:

- The insurance company will assign a claims adjuster.

- The adjuster will review the claim and assess coverage.

Documentation and Proof of Loss:

- Complete the required claim forms.

- Provide supporting documentation, like repair estimates or medical bills.

Assessment and Evaluation:

- The adjuster will evaluate the damage and policy coverage.

- They may consult experts and review policy terms.

Claims Settlement:

- The insurance company will determine the settlement amount.

- Review the offer carefully to ensure fair coverage.

Claim Payment:

- The insurance company will issue payment upon accepting the settlement offer.

- Confirm payment details align with the agreed settlement.

Follow-Up and Closure:

- Retain copies of all documents and correspondence.

- Confirm claim closure and escalate issues if necessary.

Conclusion

In conclusion, understanding different types of Insurance is essential for protecting your finances and securing your future. You can make informed decisions that suit your needs by comprehending the coverage options, considerations, and terminology. Remember, Insurance is a vital tool in your financial toolkit, providing peace of mind and safeguarding your assets against unforeseen circumstances.

Resource Hub

We hope you enjoyed this edition of our newsletter. If you found it helpful, please consider sharing it with others who might benefit from this information.

At Orelia Capital, we believe that feedback is a gift. Your feedback can help us improve our content and provide more value to our readers.