Navigating the World of Credit Cards: What 20-Somethings Need to Know Before Choosing a Credit Card.

Welcome to our comprehensive guide on using credit cards in your 20s. This article will explore the various aspects of credit card usage specifically tailored for young adults. From building credit to maximizing rewards and avoiding common pitfalls, we'll provide you with the knowledge and insights needed to make informed decisions and establish a solid financial foundation.

Understanding key terms and concepts will help you make informed decisions as you explore the world of credit cards. Here are the essentials:

- Credit Limit: The credit limit refers to the maximum amount of money you can borrow on your credit card. It is determined by the credit card issuer based on factors such as creditworthiness, income, and credit history.

- APR (Annual Percentage Rate): The APR represents the cost of borrowing on your credit card on an annual basis, expressed as a percentage. It includes both the interest rate and any additional fees or charges.

- Grace Period: The grace period is the time between the end of a billing cycle and the payment due date. During this time, you can pay your credit card balance in full without incurring any interest charges.

- Introductory Offers: Some credit cards offer introductory offers, such as 0% APR on balance transfers or purchases for a specified period.

- Annual Fee: An annual fee is a yearly charge imposed by certain credit cards for the benefits and rewards they offer.

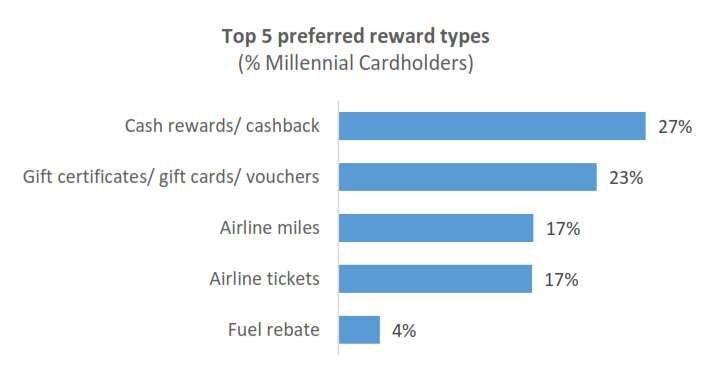

- Rewards and Perks: Many credit cards offer rewards programs, such as cashback, points, or miles, based on your spending.

- Penalty Fees: Penalty fees are charges imposed for late payments, exceeding your credit limit, or other violations of the credit card terms.

- Credit Score Requirements: Some credit cards are designed for individuals with limited or no credit history. Research cards suitable for your current credit standing to increase your chances of approval.

- Credit Utilization Ratio: Also known as credit utilization rate or debt-to-credit ratio, it is a measure that compares the amount of credit you are currently using to the total amount of credit available to you.

Building Credit in Your 20s: The Importance of a Credit Card

Building a solid credit history is essential for your financial future, and responsible credit card usage is one of the most effective tools to achieve this. Here's why building credit in your 20s with a credit card is crucial:

- Establishing a Credit History: Your credit history records your borrowing and repayment behaviour. A credit card allows you to build this history from a young age. Without a credit history, securing favourable terms or obtaining credit at all can be challenging.

- Building a Positive Credit Score: A credit score is a numerical representation of your creditworthiness. Using a credit card responsibly, such as making timely payments and keeping balances low, can contribute positively to your credit score.

- Access to Future Financial Opportunities: As you enter adulthood, you may dream of buying a car, owning a home, or starting a business. These goals often require financing. Lenders rely on credit scores to assess the risk associated with lending money.

- Improved Loan and Credit Card Options: A strong credit history opens doors to better loan and credit card options. As you build credit in your 20s, you may qualify for credit cards with higher credit limits, lower interest rates, and attractive rewards.

- Financial Independence and Responsibility: Managing a credit card teaches you essential financial skills, such as budgeting, tracking expenses, and making timely payments. It allows you to develop discipline and responsible financial habits, setting a solid foundation for a lifetime of financial success.

Managing Credit Card Debt in Your 20s: Strategies for Success

While credit cards can provide convenience, managing debt responsibly is essential. These strategies will help you stay on top of your finances:

- Track Your Spending: Start by clearly understanding your spending habits. Monitor your credit card statements and categorize your expenses. This will help you identify areas where you can cut back and make necessary adjustments to your budget.

- Create a Budget: A budget is crucial for managing credit card debt. Allocate a specific amount toward paying off your monthly credit card balances.

- Pay More Than the Minimum: Always aim to pay more than the minimum payment on your credit card statement. Paying more than the minimum will accelerate your progress toward debt repayment. By paying only the minimum, you'll pay significantly more in interest over time, and it will take much longer to become debt-free.

- Consolidate Your Debt: Consolidating your debt may be viable if you have multiple credit cards with outstanding balances. Consider transferring your balances to a single credit card with a lower interest rate or explore debt consolidation loans. This simplifies your payments and can potentially save you money on interest.

- Seek Professional Help if Needed: If your credit card debt becomes overwhelming and you're struggling to progress, consider seeking assistance from a credit counselling agency or a financial advisor.

- Avoid Accumulating More Debt: As you work on paying off your credit card debt, it's crucial to avoid accumulating more debt.

- Balance Transfers: If you have high-interest credit card debt, transferring the balance to a card with a lower interest rate can save you money. However, be mindful of any balance transfer fees and the duration of promotional interest rates.

How to Recover from Credit Card Mistakes in Your 20s

Recovering from credit card mistakes in your 20s is crucial for improving your financial situation and building a solid foundation for the future. Here are some steps to take when working towards recovery:

🟠 Assess Your Financial Situation: Start by taking a comprehensive look at your overall financial situation, including your credit card debt, outstanding balances, and payment history. Understanding the extent of your debt and financial obligations is the first step towards recovery.

🟠 Create a Repayment Strategy: Develop a strategic plan to address your credit card debt. Start by prioritizing high-interest debts, as they accumulate more interest over time. You have two popular strategies to choose from:

- Debt Snowball Method: This method involves paying off your smallest credit card debt first while making minimum payments on other cards.

- Debt Avalanche Method: With this approach, you focus on paying off the credit card debt with the highest interest rate first, regardless of the balance.

🟠 Develop a Budget: Establishing a budget is essential for controlling your finances. Take a close look at your income and expenses, and identify areas where you can cut back. Allocate a portion of your income towards debt repayment and stick to your budget rigorously.

🟠 Seek Professional Assistance: If your credit card debt becomes overwhelming or you need guidance on debt repayment strategies, consider consulting with a credit counsellor or financial advisor. These professionals can provide personalized advice, negotiate with creditors on your behalf, and help you develop a realistic recovery plan.

🟠 Negotiate with Creditors: If you're struggling to make payments, contact your creditors and explain your situation. They may be willing to work out a revised payment plan, lower your interest rate, or waive specific fees.

🟠 Avoid New Debt: As you work towards recovering from credit card mistakes, it's crucial to avoid accumulating new debt.

🟠 Build a Positive Credit History: While recovering from credit card mistakes, focus on establishing a positive credit history. Make all your payments on time, keep credit card balances low, and avoid opening new credit accounts unless necessary. Building a positive credit history is crucial for improving your credit score and future financial opportunities.

🟠 Practice Financial Discipline: Financial discipline is critical to long-term financial success. Make wise financial choices, differentiate between needs and wants, and prioritize saving for emergencies and future goals. By cultivating good financial habits in your 20s, you set yourself up for a more secure and stable financial future.

Conclusion:

Using credit cards in your 20s can be a powerful tool for building credit, maximizing rewards, and managing your finances. By understanding credit card basics, choosing the right cards, avoiding common mistakes, and being mindful of fees and security, you can harness the benefits of credit cards while establishing healthy financial habits. Whether budgeting, travel rewards, or recovering from mistakes, credit cards can support your financial goals and set you up for a successful future. Remember to use credit cards responsibly, stay informed, and continually reassess your financial goals to maximize your credit card journey.

We hope you enjoyed this edition of our newsletter. If you found it helpful, please consider sharing it with others who might benefit from this information.

At Orelia Capital, we believe that feedback is a gift. Your feedback can help us improve our content and provide more value to our readers.