Making Money Moves: Financial Planning for 20-Somethings

Your 20s can be an exciting time of life filled with new experiences, opportunities, and challenges. It’s also a time when many people start thinking about their financial future and how to plan for it. Whether just starting your career or still in school, setting financial goals and creating a plan can help you achieve the life you want. In this article, we’ll explore the importance of financial goal setting and financial planning in your 20s and provide practical tips to help you get started.

The Importance of Financial Literacy for Young Adults: Tips and Strategies

Financial literacy is the foundation of financial success. Setting and achieving your financial goals without knowing how to manage your money can be challenging.

Here are some tips to improve your financial literacy:

- Start with the basics: The first step to improving financial literacy is understanding basic financial concepts such as budgeting, saving, investing, and credit management.

- Use online resources: Many online resources can help young adults improve their financial literacy.

- Practice sound money habits: Good money habits such as saving regularly, avoiding unnecessary expenses, and paying bills on time can help young adults build a solid financial foundation.

- Read financial news and publications: Stay informed about the latest trends and developments in the financial world. This knowledge can help them make informed decisions about their finances.

- Attend financial literacy classes and workshops: Many community organizations and financial institutions offer financial literacy classes and seminars.

- Seek financial advice if needed: Financial advisors can provide personalized advice and guidance on managing finances, budgeting, and investing.

The Importance of Setting Financial Goals: How to Create a Vision for Your Financial Future

- Setting financial goals gives you direction and purpose. It helps you identify what’s important to you and what you want to achieve in life.

- Start by considering your long-term goals, such as buying a house, starting a business, or retiring early. Then break them down into smaller, achievable goals.

- Create SMART goals that are - Specific, Measurable, Achievable, Relevant and Time-bound. This will help you track your progress and stay motivated.

Creating a Budget: How to Plan Your Expenses and Save Money

- A budget is a plan for your money that helps you prioritize your spending and save for your goals.

- Start by tracking your expenses for a month to see where your money is going. Then create a budget that allocates your income towards your expenses, savings, and debt payments.

- Use apps or software to help you track your spending and automate your savings. One of the most famous budgeting rules is the 50/30/20 rule, where 50% of your income goes towards essential spending, 30% towards discretionary spending, and 20% towards investment.

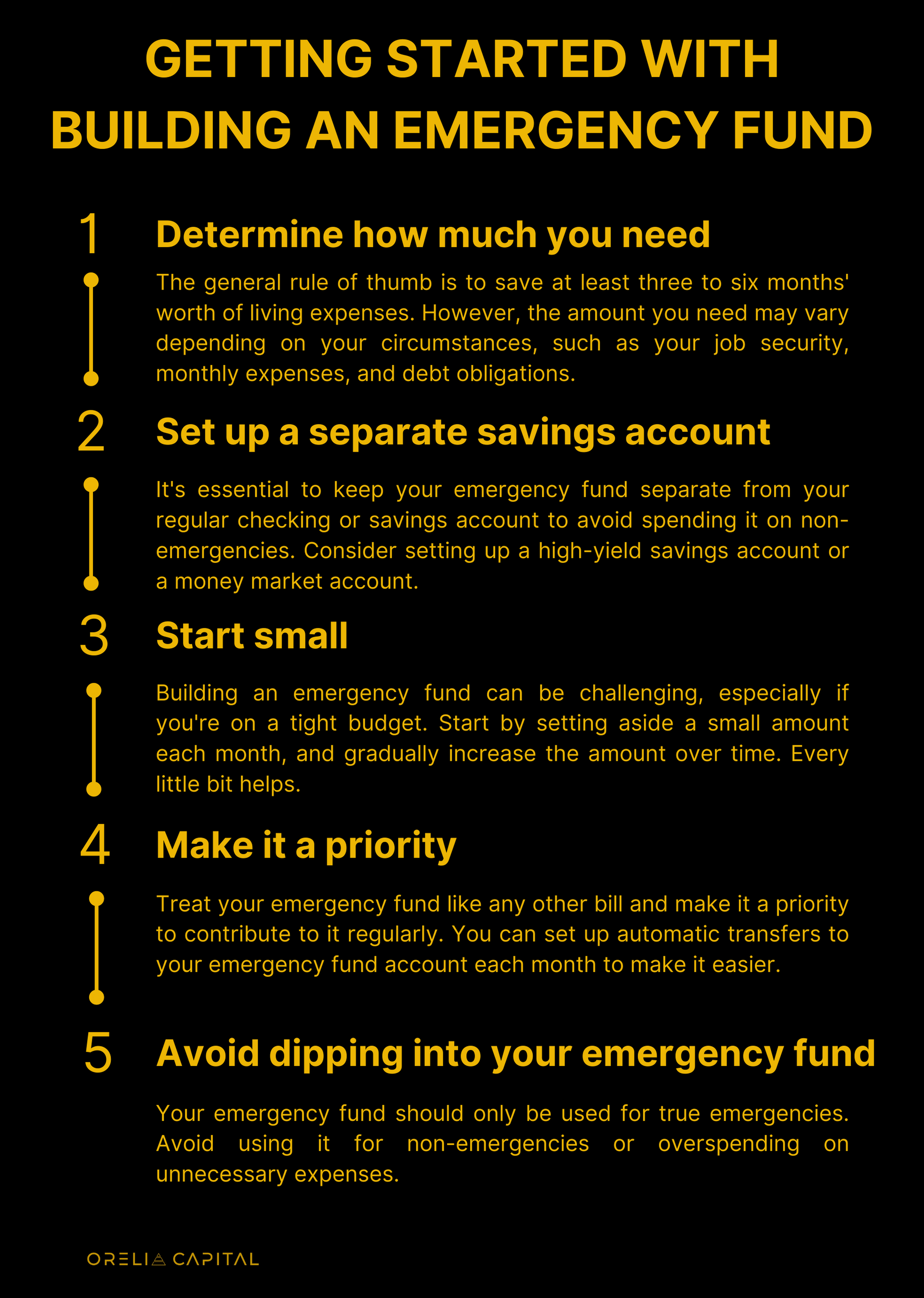

Building an Emergency Fund: Why It’s Important and How to Get Started

An emergency fund is a savings account that you can use to cover unexpected expenses or financial emergencies, such as medical bills, car repairs, or a job loss. Building an emergency fund is one of the essential steps in achieving financial stability, yet it is often overlooked.

Here are some reasons why building an emergency fund is crucial:

- Unexpected expenses are inevitable: Unexpected expenses can arise no matter how well you plan your budget. Without an emergency fund, you may have to rely on credit cards, loans, or even worse, borrow from friends or family, which can lead to more financial stress.

- Peace of mind: Having an emergency fund can give you peace of mind knowing that you have a safety net to fall back on in an emergency. You can avoid the stress and anxiety that come with financial uncertainty.

- Avoiding debt: With an emergency fund, you can avoid accumulating debt when unexpected expenses arise. Debt can affect your credit score, and you may pay more interest charges.

Saving for Retirement: The Benefits of Starting Early and How to Make the Most of Your 401(k) or IRA

Saving for retirement may seem like a daunting task in your 20s, but it’s essential to start early. The earlier you start, the more time your money has to grow. Here are some tips to help you get started:

- Start by contributing to your employer-sponsored retirement plan, such as a 401(k) in the US or a Superannuation in Australia. Contribute at least enough to get the full employer match if one is available.

- If you don’t have access to an employer-sponsored plan, consider opening a retirement account (Like an IRA in the US). Traditional IRAs offer tax-deferred contributions, while Roth IRAs offer tax-free withdrawals in retirement.

- Aim to contribute 10-15% of your income to retirement savings.

- Consider increasing your contribution rate yearly or every time you receive a raise.

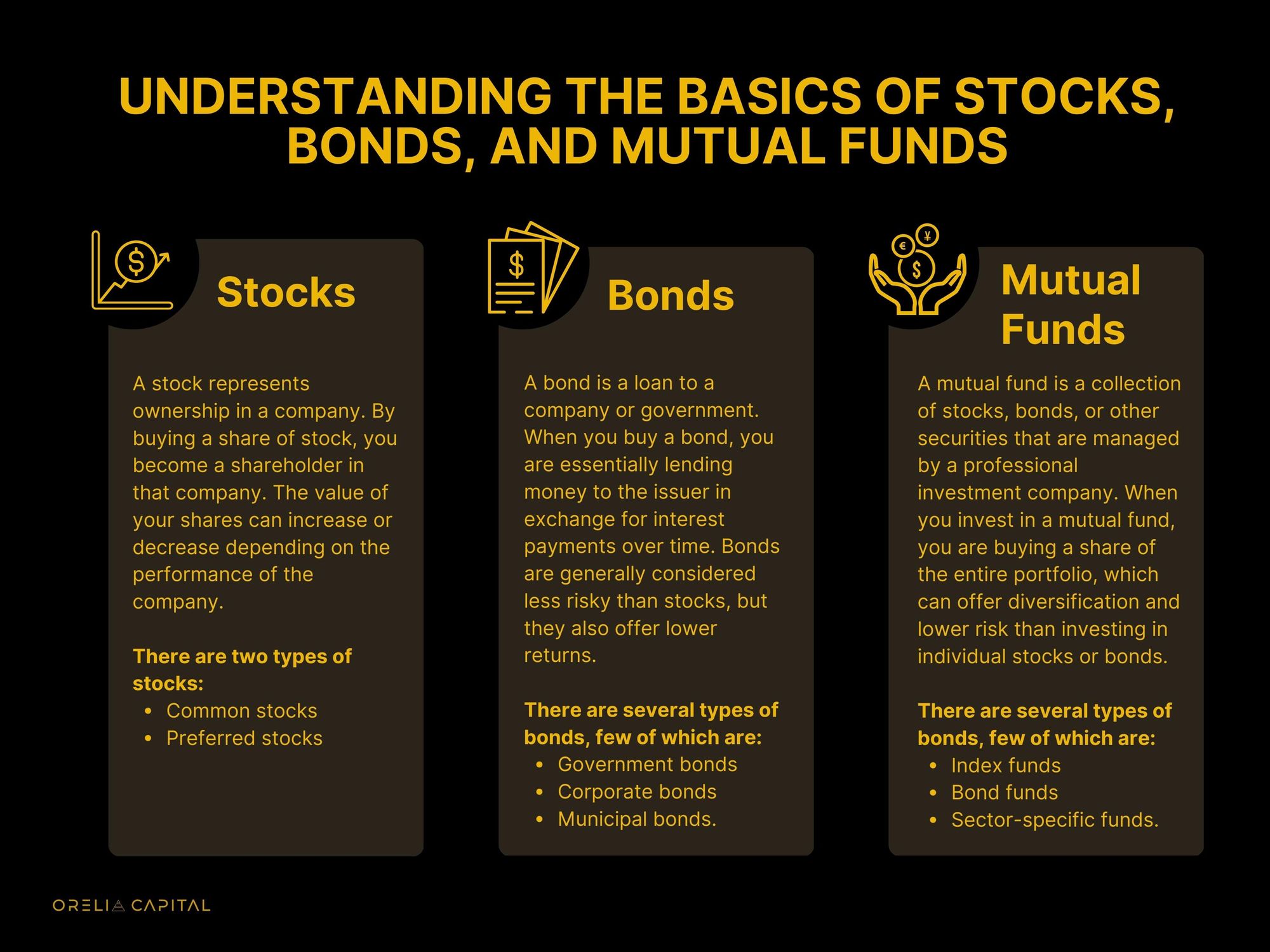

- Invest your retirement savings in a mix of stocks, bonds, and other assets based on your risk tolerance and time horizon.

- Rebalance your portfolio periodically to ensure it remains diversified and aligned with your goals.

Conclusion

In conclusion, setting financial goals and creating a plan for your future is essential in your 20s. By understanding your current financial situation, creating a budget, building an emergency fund, paying off debt, saving for retirement and big purchases, investing, tracking your progress, and seeking professional help, you can set yourself up for financial success. It’s important to remember that financial planning is not a one-time event but a continuous process. Regularly assessing and adjusting your plan will help you stay on track and achieve your goals.

Following the steps outlined in this article and staying committed to your financial goals, you can achieve financial freedom and create your desired life. Remember, it’s never too early to start planning your financial future. The choices you make now will have a significant impact on your financial well-being for years to come. So take action today and start working towards your financial goals.

We hope you enjoyed this edition of our newsletter. If you found it helpful, please consider sharing it with others who might benefit from this information.

At Orelia Capital, we believe that feedback is a gift. Your feedback can help us improve our content and provide more value to our readers.