Introduction to Bond Investing

Introduction

Welcome to this week's edition of our financial newsletter. In this article, we'll provide a comprehensive introduction to bond investing. Bonds are essential to diversified portfolios, offering a unique blend of stability and income potential. Let's dive into the world of fixed-income investments!

How Bonds Work

- Issuance: Bonds are issued by governments, municipalities, or corporations to raise capital. When an entity needs funds, they issue bonds to the public or institutional investors.

- Face Value: Each bond has a face value, also known as par value, representing the amount the issuer promises to repay the bondholder when the bond matures. Common face values include $1,000 or $10,000.

- Coupon Rate: Bonds have a fixed or variable interest rate known as the coupon rate. This rate determines the annual interest payment the bondholder will receive. For example, a bond with a 5% coupon rate on a $1,000 face value pays $50 in interest annually.

- Maturity Date: Bonds have a specified maturity date when the issuer must repay the face value to the bondholder. Maturity periods can range from a few months to several decades.

- Interest Payments: Bondholders receive regular interest payments, typically semi-annually, based on the coupon rate and the face value. These payments provide a steady income stream to investors.

- Market Price: Bond prices can fluctuate in the secondary market due to changes in interest rates, issuer creditworthiness, and market demand. When bond prices rise, yields fall, and vice versa.

- Yield: A bond's yield is the annualized return an investor can expect to earn, taking into account both interest payments and potential capital gains or losses if the bond is bought or sold before maturity.

- Bond Indenture: Bonds come with a legal contract called a bond indenture, outlining the terms and conditions of the bond issue, including the rights and responsibilities of both the issuer and bondholders.

Risk and Return in Fixed Income

Risks in Fixed Income Investments:

Interest Rate Risk:

- Risk: Bond prices can decline if interest rates rise, leading to potential capital losses.

- Impact: Investors may receive lower returns or even face losses if they need to sell their bonds before maturity in a rising rate environment.

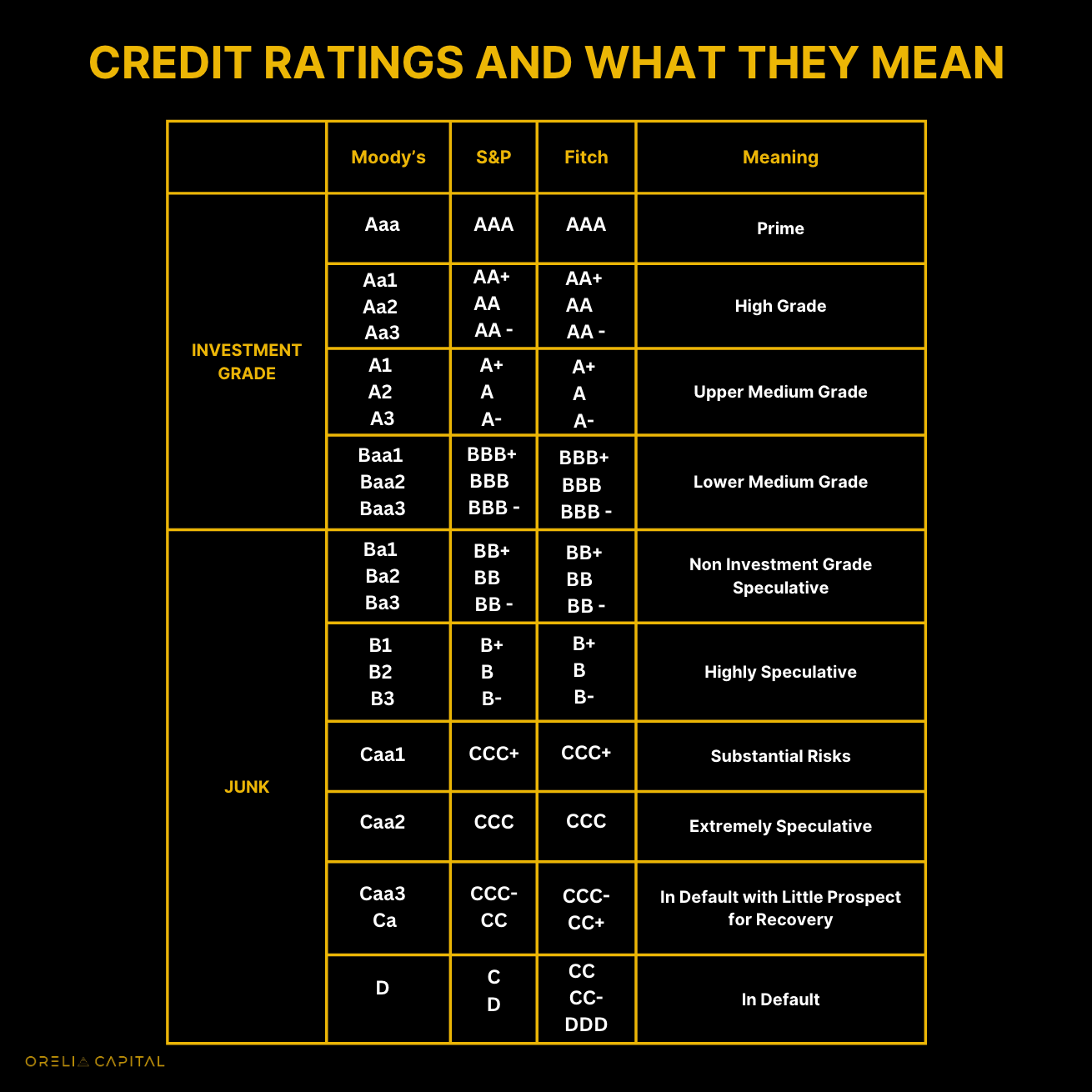

Credit Risk:

- Risk: The issuer may default on interest payments or fail to repay the principal amount.

- Impact: Investors could lose a portion or all of their investment if the issuer encounters financial difficulties.

Inflation Risk:

- Risk: Fixed-income investments may not keep pace with inflation, reducing their purchasing power over time.

- Impact: Investors may experience a decrease in real returns, potentially eroding their wealth.

Advantages in Fixed Income Investments:

Steady Income Stream:

- Advantage: Fixed-income investments provide regular interest payments, offering a predictable income source.

Capital Preservation:

- Advantage: Fixed-income investments are generally less volatile than stocks, making them suitable for capital preservation.

Diversification Benefits:

- Advantage: Bonds complement equity holdings, reducing overall portfolio risk through diversification.

Diversification Strategies with Bonds

Asset Allocation:

- Allocate a portion of your investment portfolio to bonds. The exact allocation depends on your risk tolerance, financial goals, and time horizon.

- Diversify across asset classes, including stocks, bonds, and possibly other asset types like real estate or commodities.

Types of Bonds:

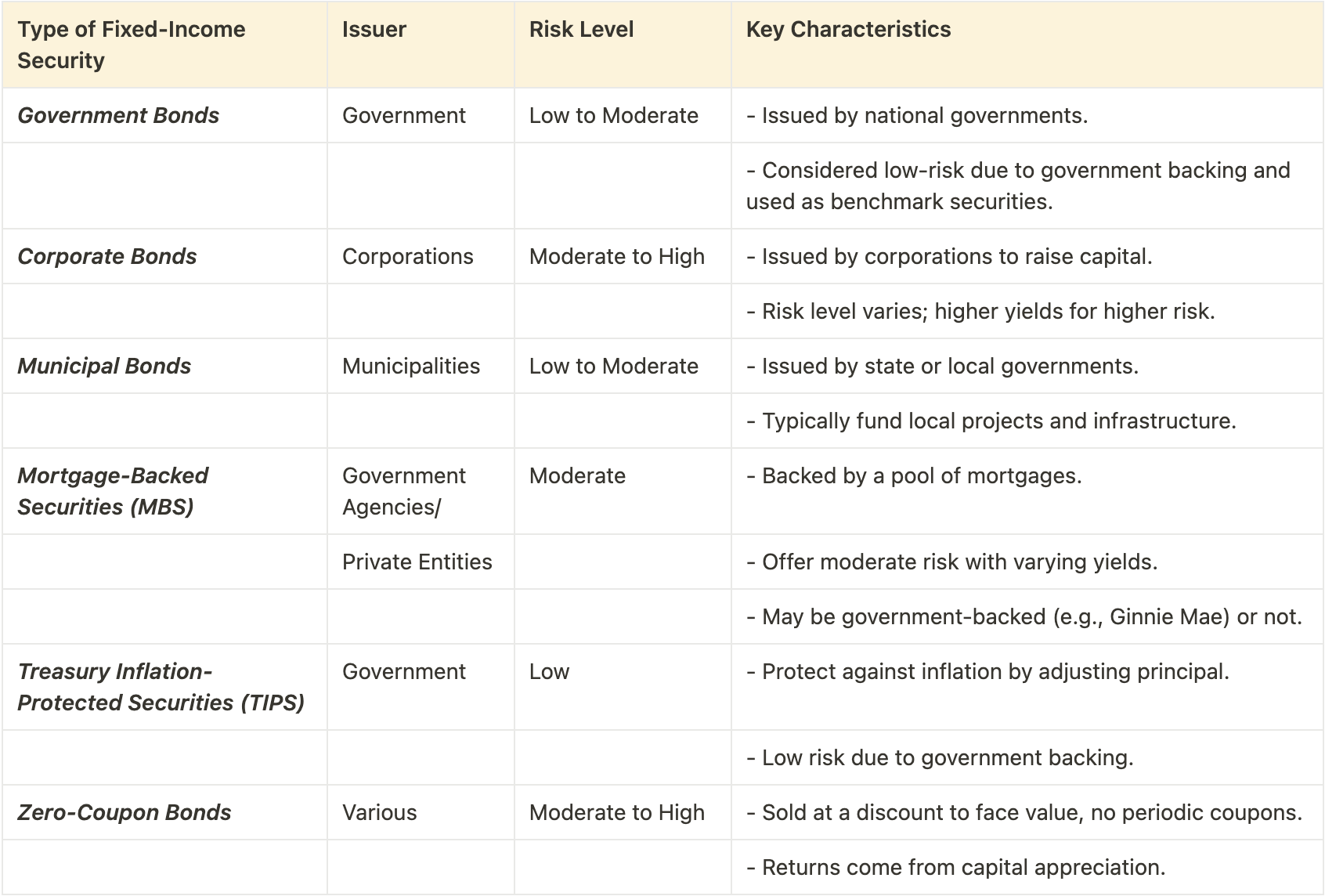

- Invest in a mix of different types of bonds, such as government bonds, corporate bonds, municipal bonds, and international bonds.

- Each bond type has its risk and return profile, helping spread risk across different issuers and sectors.

Maturity Diversification:

- Diversify maturities by investing in bonds with varying time horizons. Short-term, intermediate-term, and long-term bonds react differently to changes in interest rates.

- Short-term bonds are less sensitive to interest rate fluctuations, while long-term bonds can provide higher yields.

Geographic and Sector Diversification:

- Diversify geographically by investing in bonds from various regions and countries. This can reduce exposure to economic and geopolitical risks in a single region.

- Spread the risk by investing in bonds from different sectors, such as finance, healthcare, technology, and utilities, as the economic conditions affect sectors differently.

Consider Bond Funds:

- Bond mutual funds or ETFs provide instant diversification across a range of bonds.

- They are managed by professionals who actively select and adjust the fund's holdings to optimize risk and return.

In this introductory journey through bond investing, we've covered the essentials, from types of fixed-income securities to risk considerations and diversification strategies. Bonds can be valuable to your investment portfolio, offering stability and income potential.

Remember, while we've provided valuable insights, this article is for educational purposes only, not financial advice. Consult a qualified financial professional to tailor your investment strategy to your unique circumstances. Stay informed and make well-informed decisions on your path to financial success.

We hope you enjoyed this edition of our newsletter. If you found it helpful, please consider sharing it with others who might benefit from this information.

At Orelia Capital, we believe that feedback is a gift. Your feedback can help us improve our content and provide more value to our readers.