Financial Safety: Handling Unexpected Expenses

In the unpredictable seas of personal finance, unexpected expenses often arise like sudden storms, challenging our financial stability. Whether it's a medical emergency, unexpected home repair, or a job loss, these unforeseen events can leave us feeling financially adrift. However, just as skilled sailors navigate turbulent waters, we can equip ourselves with the right tools and strategies to weather financial storms. Money can be tricky, and sometimes unexpected things happen. This time, we're discussing how to deal with these surprises smartly.

Emergency Fund Essentials: Building a Financial Safety Net

Understanding the Significance

- Recognize the emergency fund as a crucial pillar of financial stability.

- Acts as a safety net to cushion against unexpected financial shocks.

Initiating the Fund: Practical Tips

- Start small: Initiate with a manageable amount to foster consistent contributions.

- Automate savings: Set up automatic transfers to the emergency fund to ensure regular deposits.

- Gradual growth: Aim to build the fund over time, understanding it's a continual process.

Ideal Fund Size: Three to Six Months' Expenses

- Tailor the fund size to individual circumstances, but a general rule is three to six months' living expenses.

- When determining the appropriate size, consider personal factors such as job stability, industry volatility, and family size.

Accessibility and Liquidity

- Keep the emergency fund in easily accessible, liquid accounts (e.g., savings or money market accounts).

- Ensure quick access in times of need without facing penalties or delays.

Financial Stress Reduction

- Immediate Access: Quick access to funds reduces the reliance on credit cards or loans during emergencies.

- Mental Health Impact: Minimizes stress by providing financial security and peace of mind.

Creating a Realistic Budget: Anticipating and Allocating for the Unexpected

Significance of a Well-Planned Budget

- A budget is a financial roadmap offering a comprehensive view of income, expenses, and savings.

- It provides a strategic tool to prioritize spending, ensuring financial resources align with individual goals.

Guidance on Budgeting for Unexpected Expenses

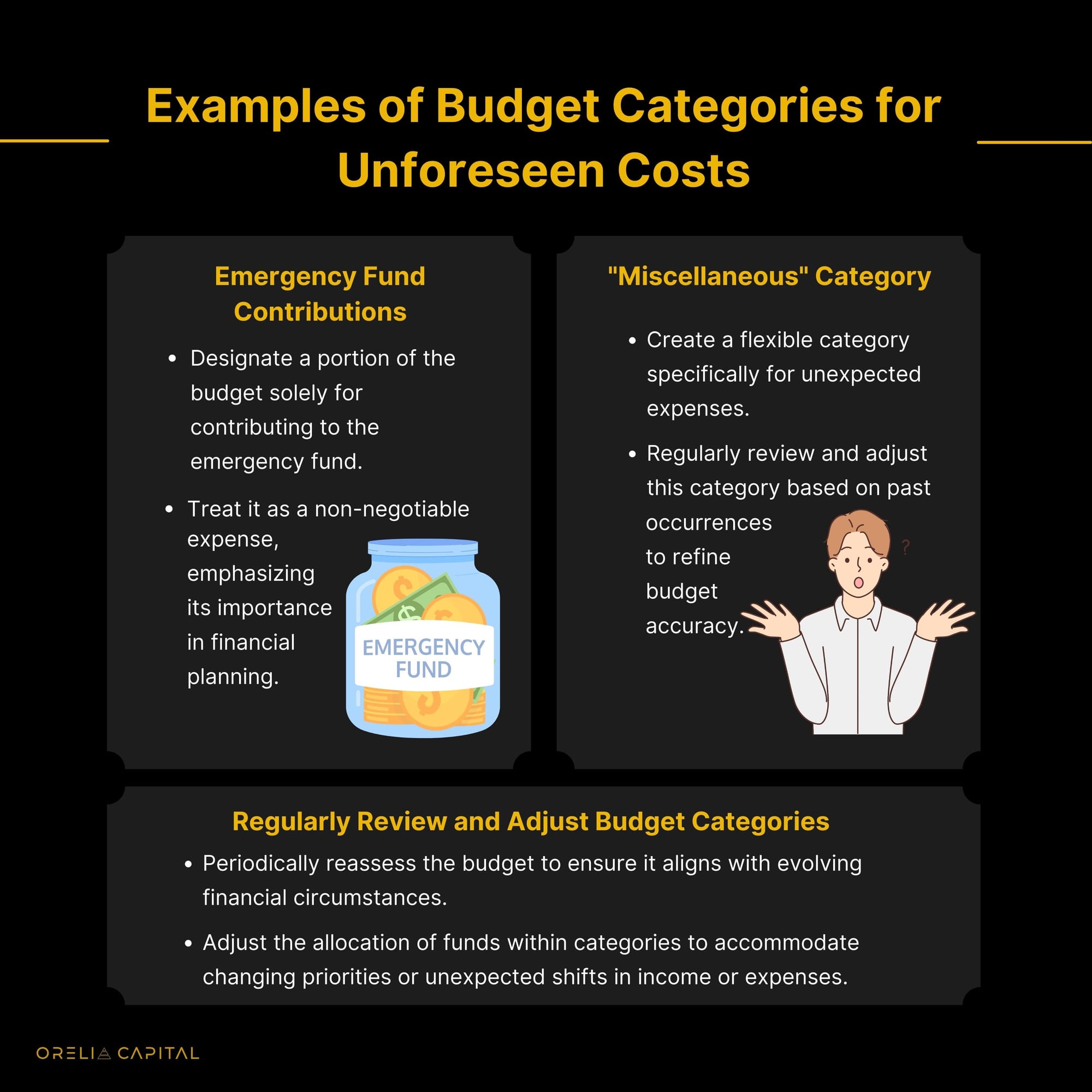

- Allocate a specific percentage of income explicitly for emergencies, typically recommended at 10-15%.

- Anticipate unforeseen costs by identifying potential categories such as medical emergencies, car repairs, or home maintenance.

- Incorporate a "Miscellaneous" or "Contingency" category to accommodate unexpected expenses that may not fit into predefined categories.

Insurance Strategies for Financial Protection:

Types of Insurance and Their Role:

- Health Insurance: Shields against medical expenses, covering hospitalization, medications, and preventive care.

- Home Insurance: Safeguards against property damage caused by fire, natural disasters, or theft.

- Auto Insurance: Covers unexpected repair costs and provides liability protection in accidents.

Choosing the Right Insurance Coverage:

- Assess Individual Needs: Consider personal health conditions, property value, and driving habits.

- Evaluate Risks: Identify risks associated with lifestyle, location, or specific assets.

- Research and Compare: Explore different insurance policies, ensuring they align with individual requirements.

Long-Term Financial Benefits:

- Prevents Out-of-Pocket Expenses: Insurance minimizes direct financial impact during emergencies.

- Financial Stability: A well-rounded insurance portfolio contributes to overall financial security.

- Protects Savings: Reduces the need to dip into savings or emergency funds for unexpected expenses.

Adapting Financial Goals: Navigating Setbacks and Adjusting Plans

Importance of Flexibility in Financial Planning

- Financial planning isn't a rigid blueprint but a dynamic process.

- Life is unpredictable; setbacks like job loss or unexpected expenses are inevitable.

- Flexibility allows for resilience and the ability to overcome challenges.

Guidance on Reassessing Financial Goals

- Regular Review: Periodically assess your financial goals to ensure they align with current circumstances.

- Adjusting Timelines: Be open to extending timelines for certain goals if needed.

- Prioritization: Identify and prioritize goals based on urgency and importance.

Conclusion

So, here's a quick wrap-up of our money journey: Keep a little money cushion (we call it an Emergency Fund) for surprise bills; we showed you how to make and follow a simple money plan (that's budget); understand different types of money shields (insurance) to stay safe; learn how talking can help you get better money deals (negotiation); and when things change, it's okay to adjust your money plans (flexibility is the key). Think of it like steering your money ship in the right direction. So, armed with these simple tools, your money journey just got easier. Sail on with confidence!

We hope you enjoyed this edition of our newsletter. If you found it helpful, please consider sharing it with others who might benefit from this information.

At Orelia Capital, we believe that feedback is a gift. Your feedback can help us improve our content and provide more value to our readers.